Insurance did not begin in a boardroom. It began with fear.

Fear of losing a ship.

Fear of fire destroying a home.

Fear of a family starving after the death of the breadwinner.

And human beings eventually realized something powerful:

“One person alone may be ruined by disaster. But if many people share the risk together, nobody has to be destroyed.”

That simple idea became insurance.

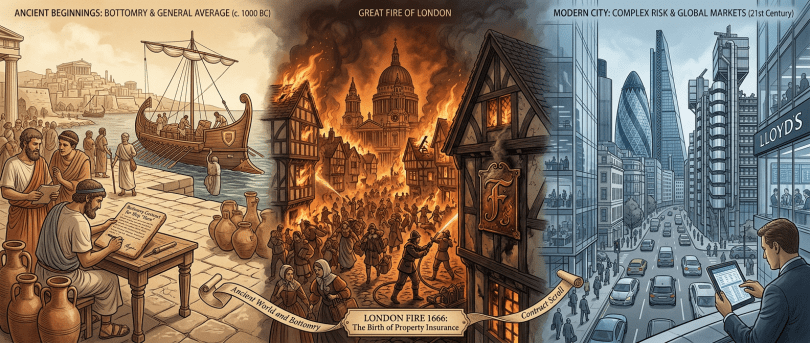

The Earliest Form of Insurance — Ancient Traders

Thousands of years ago, merchants in places like ancient China and Babylon carried silk, spices, and grain across dangerous rivers and seas.

Ships sank. Bandits attacked. Storms destroyed cargo.

If one merchant lost everything, his family could become poor overnight.

So traders created a system:

- Instead of putting all goods on one ship, they spread cargo across many ships.

- Groups of merchants contributed money into a common pool.

- If one person suffered a loss, the pool compensated him.

This was the seed of insurance.

One of the earliest written examples appears in the ancient Code of Hammurabi in Babylon around 1750 BCE. A merchant taking a loan for a sea voyage could pay an extra fee so the lender would cancel the debt if the shipment was lost.

That extra fee was basically an early insurance premium.

The Story Changes in London

The modern insurance industry truly took shape in 17th-century London.

Back then, London was crowded with wooden houses, candles, fireplaces, and narrow streets.

In 1666, disaster struck:

The Great Fire of London burned for four days.

More than 13,000 houses were destroyed.

People suddenly understood:

- Fire can wipe out entire neighborhoods.

- Rebuilding alone is impossible for most families.

After this tragedy, businesses began offering fire insurance. Homeowners paid regular amounts of money, and if their house burned down, the insurer helped cover the loss.

Some companies even created private fire brigades. Homes insured by a company displayed metal fire marks outside their houses so firefighters knew whom to help.

Shipping and the Birth of Big Insurance

At the same time, global trade was booming.

Ships traveled between Europe, Asia, and the Americas carrying tea, cotton, gold, and spices. But sea travel was extremely risky.

In a coffee house owned by Edward Lloyd, ship owners, merchants, and wealthy investors gathered to discuss voyages.

Investors would agree to cover portions of a ship’s risk in exchange for payment.

That coffee house eventually became Lloyd’s of London — one of the most famous insurance institutions in history.

The word “underwriter” comes from this practice because investors literally wrote their names under the risk agreement.

Life Insurance: A Different Kind of Protection

Eventually people asked a harder question:

“What happens to a family when a person dies?”

This led to life insurance.

At first, many people thought it was strange or even immoral to place money around death. But over time, society saw its value.

Life insurance became a way to protect widows, children, and families from financial collapse.

As cities industrialized during the 1800s:

- factory accidents increased,

- disease spread rapidly,

- workers faced dangerous conditions.

Insurance expanded into:

- health insurance,

- accident insurance,

- workers compensation,

- automobile insurance,

- business insurance.

Why Insurance Became Powerful

Insurance works because not everyone suffers loss at the same time.

For example:

- out of 10,000 homes, only a small percentage may burn down each year,

- out of millions of drivers, only some will have accidents,

- many people pay premiums, but only a smaller group files claims.

This creates a financial safety net.

At its best, insurance allows people to:

- start businesses,

- buy homes,

- travel,

- build factories,

- recover after disasters,

without being completely ruined by one bad event.

Modern economies could not function without insurance.

Banks often will not issue mortgages without homeowners insurance. Businesses cannot operate major projects without liability coverage. Airlines, hospitals, shipping companies — all depend on insurance systems.

The Human Side of Insurance

At its core, insurance is really about collective survival.

It says:

“We cannot stop bad things from happening. But we can prevent one tragedy from destroying a person’s entire future.”

That is why the concept survived for thousands of years and became one of the foundations of modern civilization.